An operating statement is used to assess a company’s performance and financial position. It is a primary financial statement, alongside balance sheets and cash flow statements.

Operating statements summarize a company's revenues and expenses for a given accounting period.

Statement of Operations vs Income Statement

Statements of operations are referred to by many names. They may also be known as:

All companies need to generate revenue to stay in business, and these revenues are used to pay expenses, interest payments on debt, and taxes owed to the government. After these costs are paid, the remaining amount is called net income, otherwise known as the source of compensation to shareholders (i.e. company owners).

Calculating Operating Statements

The basic equation on which a statement of operations is based is:

Revenues – Expenses = Net Income

Net income is theoretically available to shareholders. However, instead of paying out dividends, the firm’s management often chooses to retain earnings for future investment in the business.

Statements of operations are all organized the same way, regardless of industry.

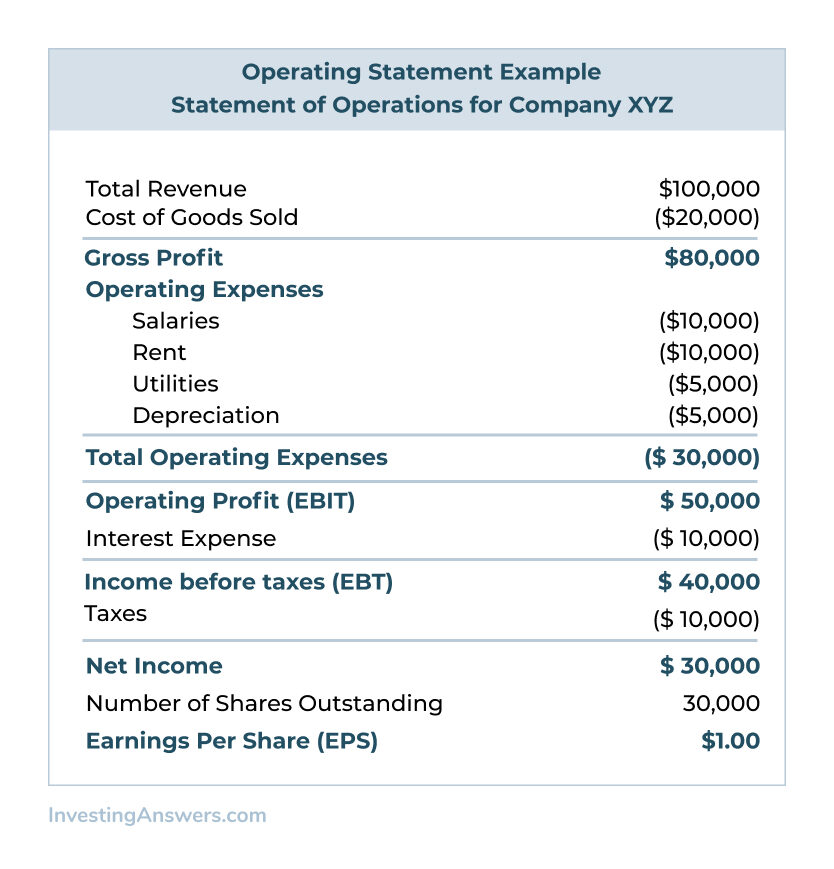

Operating Statement Example

Why Is a Statement of Operations Important?

Anyone interested in active investing, picking stocks, or investigating a company’s financial health must know how to read financial statements.

A firm’s ability to generate long-term earnings is the key driver of its stock and bond prices. Operating profit (EBIT) is the source of debt repayment, and if a company can’t generate enough EBIT to pay its debt obligations, it will have to enter bankruptcy or sell itself.

If a company cannot generate enough profit to compensate owners for the risks they’ve taken, the value of the owners’ shares will plummet. Conversely, if a company is healthy and growing, higher stock and bond prices will reflect the increased availability of profits.

Remember: Net Income Does Not Equal Cash Flow

Earnings, net income, and profits are not the same as cash or cash flow. A firm may appear profitable on the statement of operations but still not generate cash flow (and vice versa). In order to accurately view a company’s cash flow, you’ll first need to see its statement of cash flows.